{sigh} I’m supposed to be working (still!) but can’t stand another minute of it and so instead have decided to abandon my livelihood in favor of blogging. For the moment.

PF Topic of the Day: revisiting the budgeting scheme I abandoned in 20-and-aught-14. Holy mackerel, what a Year from Hell! In more ways than one: financial fiasco and healthcare fiasco proceeded hand-in-hand.

Well before a hyper-sensitive mammogram’s little discovery of an alleged one-centimeter lesion — the one that sucked me into an inescapable vortex leading to a double mastectomy for “not a cancer” — the large unplanned expenses began. Yea verily: they started in January, with surprise pool bills, plumbing bills, car repair bills, and on and on and on… Once the health-care fiasco began, I just flat gave up.

What, after all, was the point of even trying to track one crazy expense after another, let alone trying to keep them under control, when even the Mayo Clinic with all its considerable corporate power could not begin to tell me what I really owed them? They still do not know. Neither do I.

It’ll be months before enough dust settles to figure out what, after Medicare and Medigap payments, I actually have to pay toward the $60,000 or $70,000 worth of medical misadventures.

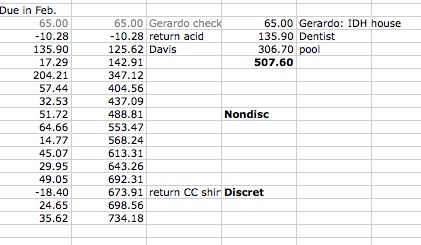

Meanwhile, I’ve gotta get back on track. So, I’ve revived the system to track monthly discretionary and nondiscretionary expenditures, in an effort to keep the discretionary spending under $1200 a month. The current iteration is slightly less onerous than previous versions: in Excel, I’m not noting the vendors that absorb my livelihood, that intelligence, after all, being redundant with the data recorded in QuickBooks. All the new tracking system shows is each expenditure and the running total.

Last month I did pretty well: only $955 in discretionary expenditures — well under budget! — and $74 in extra water charged up by draining and refilling the pool. Not bad. This happened because I was flat on my back in bed most of the month.

As for February? Welll…..we seem to be making up for lost time.

Extraordinary expenses are freaking through the roof: $65 to the yard dude for service above and beyond the call of duty at my son’s house; $136 to get my teeth cleaned; $307 to clean the pool filter and repair a part the disgraced Pool Dude probably broke. Holy shit: we started out $507 into a budget of $1200 (which we’d like to keep down to $1100 if at all possible)! It’s gone downhill from there.

With $507 of extraordinary expenses and $734 of normal discretionary expenses, I’m already more than $40 in the hole: and 16 days remain to go in the discretionary budget cycle. By the end of February, mercifully a short month, I am going to be deep, deep in the red.

As yet no paycheck from Heavenly Gardens Community College, even though we’re into the third week of the semester. The joys of adjunct teaching.

Yesterday I bought gasoline, probably enough to last until the new AMEX cycle kicks in (not shown in these figures…). But clearly I can’t do without at least one or two grocery store runs between now and the end of the month. And we’re running low on dog food: that means I’ll have to go into Costco to pick up more large packages of chicken or pork to make new food, which I believe to be healthier for the dogs and cheaper than the closest commercial approximation of Real Food for dogs.

I’d planned to make one, count it (1) Costco run per month, limiting the $200 trips to that Emporium of Impulse Buys, but if that is to happen, I’ll have to buy twice as much dog-food meat per trip as I’ve been accustomed to purchasing at any given time. Even this, though, may prove cost-effective: every time I go into Costco, I come out with my bank account several times lighter than expected. In any given month, the fewer C0stco visits, the closer I come to ending on budget. So, even if I buy more of X product category in a given trip, stocking up on enough to head off a second trip that month will save money.

This month’s utility bills have yet to come in, of course, it being only the seventh. But in a February, power and water bills should both be fairly low, well under the $660 nondiscretionary budget. So with any luck the total discretionary + nondiscretionary should not exceed the total planned $1860 by very much. I hope.

But…the only way to keep within this limit, as the weather grows hotter and utility bills bloat accordingly, will be to keep a grip on grocery bills and the various nasty little surprises.

$1,860, by the way, is about $660 more than Social Security pays. Social Security is my only consistently reliable income source, adjunct teaching being the joke that it is.

Not good, is it?

Well, after reading the blog, I can see that you didn’t actually add poo to the water. Whew.

Is there a reason you paid for the pool work for your son? I know he’s super-son and you must have a reason, but had to ask. And if I remember correctly, you have retirement investments, you’re saving them for when the teaching ends? Or could you tape them now?

$1,200 is not much for discretionary though you seem to be able to manage within that number. Could you downsize and tap some home equity?

Poo to the water? where does it say that? My search program is not bringing up anything like that. Ohh…I see: the “grab” program cut off part of an Excel cell. Sorry about that. 😀

Pool work? No, I paid to have the yard man trim a large, out-of-control carob tree. My son paid for him to shovel out the back and front yard, cut back a dozen frozen bougainvilleas, repair dog damage, and cetera. There’s a limit to how much he can afford, and I felt we were likely to get a better result on the appraisal for refinancing if we could get the front looking better. The difference could be several thousand dollars in our favor…or otherwise.

On your excel file it appears (at least on my laptop) to say

“extra water: poo

added into water”

LOL!

Oh…also not explained clearly: The appraisal for which we did the clean-up job was part of a refinance project that will get us out from under an onerous balloon payment that looms ahead of us, and also to drop the interest rate from 4.5% to 3.8%.

Gotcha

Gotta love the “balloon payment”. In another life I sold real estate and those 7/23 and 5/25 products were like “manna from heaven”. And the interest only with the balloon enabled many a customer to get into more house than they could otherwise afford. Hopefully that’s not what you had with your son’s property. As memory serves it get’s crazy quick.. if and when you don’t come up with the balloon and/or the property doesn’t appraise. Good Luck on the refi 3.8 sounds like a decent rate… Just watch for the “junk fees” on those refi’s…that HUD 1 can be a minefield…

It actually was a 30/15 loan: The payments were what they would be on a 30-year term, but the loan came due in year 15. At that time we would have to refinance.

At the time we bought the house, we thought the market was reaching the bottom. I figured the house’s value would drop as much as another 10 grand and then, within two to four years, recover the value that we had paid for. The neighborhood is uber-ripe for gentrification — and in fact, as we scribble it IS gentrifying — and so we thought that if my son stayed in the house to 2023, he not only would have a pleasant place to live but we would make (maybe) a small profit. At worst, we thought we would break even. While neither he nor I thought he would stay in the house for 15 years, we expected that if he did, by year 15 the principal would have been paid down and value would have risen to the point that it would have been worth refinancing if he wanted to stay there.

Talk about WHERE’S YORE SIGN?!!

Even though I personally anticipated a recession, I don’t think any of us lowly middle-class types could have understood that we were headed to the brink of a major economic depression. Neither did our Realtor, who in addition to being a very smart gentleman with an MBA and a long career in business behind him, happened to be a friend.

Hmmm….Is your friend with the MBA still a Realtor? My experience with highly educated real estate agents was not pleasant more times than not. It seems “they had it all figured out” and actually did not. This wasn’t “rocket science” and folks tended to make it more complicated than it needed to be… The scenario you are describing was known as ….”selling the sizzle rather than the steak”…selling what COULD be rather than what is…Good luck on the refi….

Yeah, he’s still in the real estate biz. He also about lost his shirt, having invested in a couple of rental houses himself. But he managed to hang in there.

He’s an older man who had retired, with his wife who also had been a marketing executive but who was younger than him. She decided she wanted a child, so now they have a little girl that he dotes on. But he realized that with a kid to send to school they would need an active income again, so he decided to try real estate. Says he loves the business but has never worked harder.

Don’t think he’s ever claimed to have much of anything figured out. 😀 He just works hard and hopes for the best.

Things have turned around here in lovely uptown Arizona. Property values have returned to where they were before the wacko boom, and many houses are worth almost as much as their “balloon” value.

Some fix-and-flippers bought the house next door to my son’s, which was occupied by someone who supposedly was an original owner but IMHO was too young for that to be possible — probably, like a number of folks down there, the offspring of an original buyer who grew up there and then inherited the house. They paid pretty close to what I would call market price for the place and are madly renovating.

Probably if we could have waited until they could sell the place, we’d have had better comparables…but by then, I expect, interest rates will be rising.

Others on his street have been fixing up. Though a few houses are still rentals, they’re at least decently maintained. It’s a pretty little neighborhood, centrally located and within walking distance of the lightrail.

The pattern in central Phoenix has been for older neighborhoods with “charm” (which these houses have in spades) to be discovered by gays and young, childless professional married couples, who run amok fixing them up. There now are several “historic” neighborhoods in the central part of the city whose values are amazingly inflated.

Phoenix is a city made up of inconsistent “pockets.” Because wages are generally low here and because the government is controlled by people who think it’s all your personal fault if you’re poor and so work to punish the working poor, overall SES is fairly low. So you have a sea of crime-ridden low-income housing that’s interrupted by enclaves of affluence, sometimes startling affluence. Some rich people, mostly doctors and lawyers, don’t enjoy commuting and are willing to pay handsomely to avoid it.

That’s why my neighborhood is the way it is: million-dollar houses within walking distance of a dangerous meth slum. Just about all the central-city Richerati enclaves are surrounded by questionable and even dangerous tracts. It’s the result of short-sighted, often stupid political leadership…fed, I suppose, by greedy developers and ill-educated voters.

Are you aware you referred to last year as 1914?

Meds? 😀

Hm. Must have been the Eau de Bourbono meds!

Hmmmm…..Greedy developers? YIKES…..Actually one hand washes the other. You get a developer with a great idea to build a development/project in a ….”challenging” environment/neighborhood. To do so and take the risk he/she will need guarantees or “help”. This worked well in Baltimore with the Rouse Company developing the Inner Harbor and beginning a “re-birth” of sorts. The city soon started the $1 house campaign. That’s right you could buy a house for a $1….and there were caveats….BUT those same $1 houses now fetch $600-750K. Glad to hear your area is recovering. In this neck of the woods the recovery is “selective”….Modest house down the street from me just sold for $350K…in a day…however where my 1st rental is located a house just sold for $45K….these areas are 9 miles apart.

Actually, what’s done the most harm here has been sprawl: blading the desert at the rate of an acre an hour to transplant families into vast ticky-tacky, look-alike warrens halfway to Yuma, with hideous gas-guzzling commutes facilitated by godawful homicidal freeways that do as much damage to the irreplaceable Sonoran desert as do the ugly tracts themselves.

This has happened because the City Council and the Maricopa County Board of Supervisors are heavily larded with wealthy developers, whose agenda in fact IS to promote far-flung development and shovel the middle class out of the central parts of the city. They make no secret of this.

Wealthy people who don’t want to fight City Hall move to north Scottsdale and resign themselves to lengthy commutes — or engineer various telecommutish arrangements with their employers. Wealthy and upper-middle-class people who can afford to put their kids in private schools and pay a premium to live in a decent centrally located neighborhood populate gentrified “historic” and mid-century neighborhoods inside the Phoenix city limits. Middle- and lower-middle-class families who need to put their kids in public schools are forced to move to distant, ugly suburbs and accept long, unpleasant daily drives, whether they like it or not.

And poor folks who can’t afford to buy $200,000+ housing fill the increasingly slummy, aging apartment houses and worn-out 1950s to 1970s middle- and working-class housing that makes up most of the area between about 16th Street and, say 60th Avenue, between South Mountain and the North Mountain Preserves.

Developers who do infill along the Central Corridor, which was always affluent and is now increasingly so, build the occasional tract house on an empty lot and sell it for $700,000. (In my ‘hood, this was accomplished most recently by tearing down a unique architect-designed mid-century modern house on a half-acre and jamming four ticky-tackies onto the land.)

There’s a lot of money to be made in infill and renovation, but it’s not as profitable as building a stick-and-styrofoam tract, because the land isn’t cheap, the infrastructure is old and needs to be brought to modern code, and you have to do battle with the neighbors and with city codes that include set-backs and other issues that might put a crimp on your style.

The affluent professional class that actually WANTS to revive the central city (for selfish reasons, despite altruistic trumpeting about historic preservation, public transit, and green living: they want to live close to work) has put up a fight. This war of the wills has been going on for decades, and of late we’ve seen some progress. The city’s downtown has largely been revived, mostly because Arizona State University built a satellite campus there, complete with dorms and apartments that brought a lively set of young people into the area. The city has thrown off the old race-based bussing laws and allows parents to send their kids to just about any public school they can get into. Plus we now have quite an array of charter schools, a few of which are more or less decent academically. This means that many couples who can’t afford private schools now can move into the central city and plan to raise families here.