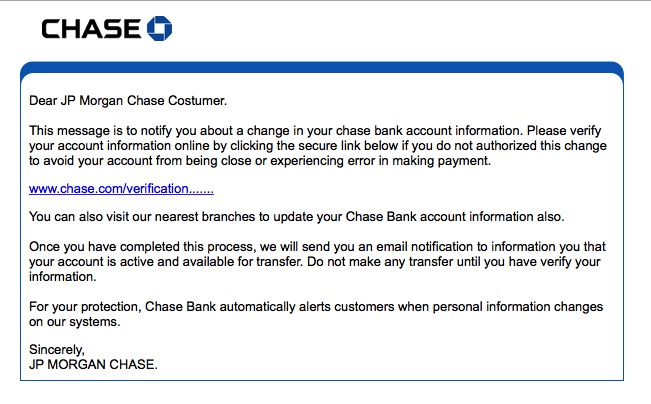

Do you or do you not just LOVE this? Supposedly from Chase Bank:

“if you do not authorized this change…” “your account from being close or experiencing error…” “until you have verify your information…”

ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha ha !!

Where do you guess it came from? China or Russia?

My bet’s on the Russians: the unfamiliarity with the use of articles with nouns is a clue (a native speaker of English would say “an error” or “errors”). Most halfway decent Chinese ESL speakers get the verb tenses down pretty well: “do not authorized” and “you have verify” are atypical, but on the other hand, Russians can usually get Western European verb structures better than this.

Let’s toss Africa into the mix, too. “Once you have complete this process, you will transfer $10,000 to our account in Nigeria so Prince iBangiBangi can succeed to his throne, at which time he will bestowing the $1 million reward upon you via Western Union…”

In a moment of idleness, I decided to Stumble in search of sites that might interest friends of Funny about Money. Below, 25 sites full of information, leads, and tools for personal finance enthusiasts. Prepare to bookmark!

Find Help, Get Action:

Hard-to-find 800 numbers. Includes Amazon, Google(!!), Dell, Apple. Some entries give a clue to how to reach a human.

Consumer Action. Free hotline refers consumers to complaint-handling agencies through our free hotline. This nonprofit publishes multilingual educational materials; compares prices on credit cards, bank accounts and long-distance services; advocates for consumers.

Federal Reserve Consumer Help. Contact the Federal Reserve if you’re having a problem with a bank or other financial institution.

General Consumer Information

Lifehacker. The Magic 8-Ball of interesting, useful, and amazing stuff

Federal Citizen Information Center: a gold mine of information. Click “Employment” to check out “how to get a job in the federal government.”

FRB Consumer Information. Another Federal Reserve Board page: banking, credit, mortgages, personal finance, leasing, identity theft. Useful information.

Consumer Reports on privacy. What information is being collected about you, why you need to know, and what (if anything) you can do about it. Did you know there’s a database tracking your record of returned merchandise?

Radio frequency identification. Clear, readable, and well researched excerpt from a law review article detailing what this is and how it will affect everyone’s privacy. Even cash transactions will be trackable…right to your doorstep. So much for any ideas about “going off the grid”!

Pest Control

Spambox. Creates a temporary e-mail address for those outfits that demand an e-mail address to “verify” when you need to download or get into a site. It forwards to your real site and then expires after a set time.

Bug Me Not. Shared logins for sites that pester you to register

Annoyance zappers. Plug-ins for zapping many common online annoyances

In a history article for a client journal, one of our authors mentioned Measuring Worth, a nifty tool that allows you to compare a variety of money-related values over periods stretching back to 1774. Among other things, it will calculate the relative worth of the dollar. Enter a specific sum and a year, and then ask what it would have been worth in a later year. The engine disgorges the equivalent according to six different indicators: the consumer price index (CPI), the gross domestic product (GDP) deflator, the consumer bundle, the unskilled wage rate, the GDP per capita, and the GDP.

The first two are ways of measuring average prices. The third (consumer bundle) shows the average value of a household’s annual expenditures; the unskilled wage rate provides a way to compare wages over time. The GDP per capita is another way to compare income over time, and the GDP itself, the market value of all goods a country produces in a year, shows “how much money in the comparable year would be the same percent of all output.”

More on this feature in a minute.

First, though, let’s look at a feature of special interest to personal finance enthusiasts: Measuring Worth also has a tool that shows how much savings would have grown over time. Enter a value and a date, and then ask how much that value would be worth at another date (up to this year), and it will tell you the return on a short-term investment, a long-term investment, and a stock market investment.

So…let’s say your child is 19 years old now, and you’d like to send her to college. When she was born, in 1990, your parents gave you $1,000 to invest toward her education. If you’d put the money in an excruciatingly safe short-term asset, today it would be worth $2,060. Invested in a long-term asset with a term of 20 years, it would have yielded $4,973. And had you put it in a Dow Jones Average portfolio, you would have $4,196, a middling performance.

Well, what if your own parents gave you $1,000—say, when you were born—and now you’re about to retire? If you were 65 today, the gift would have come in 1944 (and it would have been a lot of moola in those days!). Assuming you kept that investment separate and didn’t add more cash other than reinvesting proceeds, how far would it go today toward supporting you in your old age?

Whoa! Over a really long term, the stock market beats the other two investment modes, hands-down.

I wonder how our college girl would’ve been doing before the Bushies screwed up the economy. How much would her stock portfolio have been worth a couple of years ago, when she was 17?

Ah hah! $4,918. In the stock market, her savings would have fallen off $722 over the the year between 2007 and 2008. In a long-term investment instrument, it would’ve been worth $4,549 in 2007, $424 less than the most recent value. It appears that given competent national leadership that recognized the importance of regulating financial markets and was capable of an intelligent response to 9/11, she might have been better off in stocks and bonds.

Entertaining, isn’t it?

Now for the money story:

At the time my father was born, in 1909, his mother had about $100,000. She’d inherited this small fortune from her father, who had made it freighting buffalo hides out of Oklahoma into Texas. Also at about the time my father arrived, her husband ran off. He eventually was found dead by the side of a rural Texas highway. This left her alone with an infant, a change-of-life baby. My father had two elder brothers, the youngest of whom was 18 years older than he was. By the time he was born, both men were out of the house with families of their own.

She became involved with a Christian church on the fringes of mainline Protestantism, and she also became interested in spiritualism. She donated copious amounts to both causes. By the time my father was about ten years old, these worthies had sheared her of every penny that she had. She was left destitute.

Her home was taken away for taxes. She also lost a commercial property and another house she owned. The two older brothers, who knew nothing of this until they returned home and found her on the street, fell out over the fiasco. Tom, the eldest, was a ranch foreman who, of course, lived out in the sticks. He felt his middle brother, Ed, who lived in Fort Worth where their mother lived, should have been keeping an eye on her finances. The brothers were permanently alienated as a result of the bad feelings that arose in the wake of their mother’s impoverishment.

My father also was permanently affected. He developed a lifelong hatred of organized religion (his skepticism—shall we say—is the reason that to this day I will not donate to a church), and he also conceived a passion about money. He decided that, as his life’s goal, he would earn back the hundred thousand dollars.

And he did.

You understand, he was not a sophisticated man. He dropped out of high school in his junior year, lied about his age, and joined the Navy. He went to sea all his adult life, ultimately became a master mariner, and retired at the age of 53, when he achieved his goal of accruing $100,000 in savings. Details like the relative value of money were largely beyond his ken. Though he understood that a hundred grand didn’t make him a wealthy man in 1962, he had no way of anticipating the double-digit inflation of the 1970s. By the time that was over, the nest egg that would have kept him comfortable wasn’t worth enough to support him through his old age in a fashion other than basic poverty.

Luckily, he was a very frugal man by nature, and so it didn’t much matter: his lifestyle wouldn’t have changed, one way or the other.

I have always wondered what that $100,000 of 1909 would be worth in today’s dollars. Let’s enter it and the date of my father’s birth into the Measuring Worth relative value calculator. Current data, we’re told, are available only up to 2008. According to the various measures, today the dollar value of her inheritance would be…

• CPI: $2,441,007.10 • GDP Deflator: $1,777,507.10 • Value of consumer bundle: $5,009,823.18 • Unskilled wage: $10,307,228.92 • Nominal GDP per capita: $13,314,632.87 • Relative share of GDP: $44,808,290.00

In terms of purchasing power, my grandmother’s hundred grand would have been worth $2,441,077.10 in 2008. LOL! Think of the McMansion I could’ve bought with that as a down payment!

What if she had put her inheritance in the stock market, instead of diddling it away on her religious delusions? Invested in a nice, balanced portfolio, by the end of 2008 it would have been worth $16,595,085.85.

Well. Any way you look at it, if she been a little smarter about money and a little less inclined to woo-woo, today I wouldn’t be worrying about how I’m going to get by in retirement!

My father hugely underestimated the amount he would need to live comfortably into his mid-80s. Of course, without his mother’s crystal ball he couldn’t have anticipated the inflation that ate up his savings…but I think, given the way the government is spending money in the wake of the crash of the Bush economy, we can expect a similar inflationary period in the near future.

How much would I need in savings to have the equivalent of the $100,000 he had managed to earn back by 1962?

• CPI: $711,510.24 • GDP Deflator: $569,106.07 • Value of consumer bundle: $879,310.34 • Unskilled wage: $809,366.13 • Nominal GDP per capita: $1,510,749.04 • Relative share of GDP: $2,465,665.02 • Purchasing power: $711,510.24

Hm. If the least of these—$569,106.07—is what I’ll need to survive in moderate comfort (or not!), then I’m in deep trouble. Eighteen months ago, my savings were close to that. But today they sure aren’t, thank you very much, George and friends!

Welp, too late now. There’s not a thing I can do about it, so there’s no point in fretting. Tra la!

Michael Florek

General Manager Scientific American

415 Madison Ave.

New York, NY 10017

Dear Mr. Florek:

I believe your circulation department finally succeeded in snookering me with its flurry of hysterical “your-subscription-is-expired” mailings sent months before the real expiration date.

Because this dishonest tactic has become the custom in magazine fulfillment, I started using an Excel spreadsheet to keep track of when I actually pay for subscriptions. However, your flurry started before December, and in the holiday rush I neglected to look up the last date I paid.

Note the enclosed, stating that my subscription has “officially expired,” which arrived last month. Don’t think so. A belated look at the spreadsheet (also enclosed) reveals that I paid for a year’s subscription on 2/20/08. This means that at the time I sent you another check, on 12/9/08, my subscription still had almost two and a half months to run!

This is a rip-off, and I highly resent it. I work for a university, and believe me, my friend, I am not paid what some publishing executive on Madison Avenue earns. I cannot afford to be gouged two or three months in advance for a bill I do not owe.

If you want to keep me as a subscriber, you need to credit me for the extra two months and 11 days I’ve paid for. I will resubscribe (maybe) in February of 2010, which is when the two subscriptions I now own will expire.

You and your fulfillment contractors should be ashamed.

Sincerely, (etc.)

Attached: Letter from Mr. Florek exclaiming the subscription expired, received in December

Excel spreadsheet showing payments on 2/20/07, 2/20/08, and 12/9/08

Well, here’s one of the problems of senility: if your notes to yourself are to work, you have to readthe notes! You can’t read notes to help you remember things unless you remember to read the notes.

“YOUR NEXT ISSUE WILL BE YOURLAST ISSUE!IT’S ALARMING BUT TRUE…UNLESS YOU RENEW NOW!”

This message comes plastered to the current issue of Consumer Reports, the widely respected (off and on) self-appointed guardian of consumer interests.

Alarming, indeed, but is it true?

Well, no. My bill isn’t due for another three months. I paid for a one-year subscription in March, 2007. For this “alarming” message to reach me on January 5, it would have been mailed in December, four months before the actual renewal date.

Magazine hustlers—the august Consumer Reports included—rely on the twin probabilities that you don’t recall when you paid and that it’s more trouble than it’s worth for you to dig out your records to find out when you did pay. So you’ll pay a few months early. Each year you pay another month or two or even three early, and guess what-after a very few years, you’ll have paid for an extra subscription. An extra ten thousand $20 subscriptions represents a free $200,000 for the magazine. Sweet, eh?

A couple of years ago I realized my magazine subscriptions were coming due within a month or two of each other, after I had deliberately signed up for each at different times of the year so that I could afford to pay for the subscriptions without straining my budget. A Quicken search revealed that, yea verily, renewal demands were coming months ahead of the actual renewal dates.

If you have Quicken or a similar program, here’s an easy way to keep track of when subscriptions are actually due:

When you pay to renew a subscription, enter the amount you paid and then make another entry for the same month and day, one year in the future (or two or three, depending on your subscription’s length), showing when the renewal is due. For example, the account I use to pay subscriptions shows these entries:

1/7/08: Harper’s due

2/10/08: Scientific American due

2/10/08: Atlantic due

3/6/08: New York Review of Books due

3/6/08: Consumer Reports due

9/1/08: CR Money Advisor due

11/20/08: gift sub for Atlantic due

The reason two subscriptions are due in February and two are due in March—when I would never start two subscriptions in one budget cycle—is that I didn’t realize I was being herded into paying earlier and earlier until the due dates had been pushed forward, closer and closer to the beginning of the year, and finally began to coincide.

Just because a publication’s editorial policy seems sound does not exempt its circulation department from sleaze. Keep your eye on the rascals…no matter how venerable or upstanding the journal’s reputation!

“if you do not authorized this change…” “your account from being close or experiencing error…” “until you have verify your information…”

“if you do not authorized this change…” “your account from being close or experiencing error…” “until you have verify your information…”