So step one for the new Re-Budgeting Scheme is now accomplished.

If I’m gonna start budgeting again, I’m gonna need to have a budget. So it’s off to Excel, the classic tool of the numerically obsessed and the arithmetically challenged.

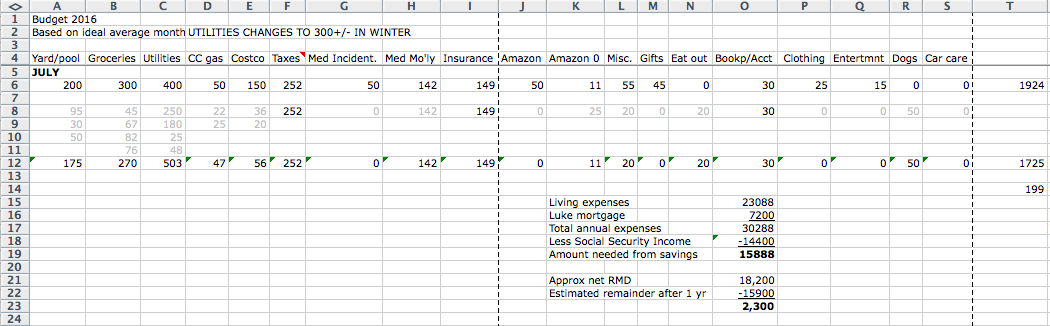

In this draft of the new scheme, monthly figures are arranged horizontally, rather than in a single column per month. This JPEG may not be very scrutable on a web page; try clicking on it for an enlarged version.

The header row lists all the spending categories that consume my annual mite. Some of these things are paid annually: taxes, for example, homeowner’s and auto insurance, and some of the healthcare policies. Even though they’re actually paid when they come due, in order to account for them, they’re prorated monthly. Effectively the money is not available for monthly spending, even though it’s in the bank.

The greyed-out figures in this image are theoretical entries, since July has yet to occur. The bottom line (row 12 here) will represent the amount spent in each category in a given month. The figures on the far right total, horizontally, the amount available (row 6) and the actual amount spent (row 12). The bottom figure in column T ($199 here, as an example) represents the difference between row 6 (amount available) and row 12 (amount spent).

We shall see if that latter figure is ever expressed in positive numbers….

Utility bills will drop to around $300 in the four winter months. They probably will exceed $400 this month and next, given the early heat and now early humidity. And unless we get some old-fashioned summer afternoon rains — which we rarely see anymore, thanks to the paving over of paradise — the water bills also will exceed budget between now and September.

All told, estimated living expenses should add up to about $23,100 annually. The mortgage on the downtown house, which my son and I are copurchasing, runs $7200 a year, for a total of about $30,300 a year.

Alas, Social Security covers less than half that.

Net RMD (required minimum drawdown) from the big IRA is a little over $18,000. I’d prefer not to use that to live on, but it looks like there’s no choice. So, unless living expenses can be cut, the net amount left at the end of the year should be around $2,300.

Not great… I’d hoped to be able to reinvest a fair amount of the RMD, but evidently that’s not going to happen unless something upward of 10 grand can be withdrawn from the S-corp. This will require a lot more editorial work to come in.

So… Can savings be found in this budget, without having to sell the house and move to abhorred Sun City?

To start with, I expect the Costco bill will drop significantly. I’ve canceled the unwelcome Citibank Visa cards, which will require me to write a check or use a debit card to shop there. The extra hassle will be enough to discourage casual shopping there. After this, I’ll go into the store only to buy a few very specific items that are hard to find elsewhere.

This afternoon I bought a $50 cash card at Costco to cover next month’s gasoline, so I won’t have to use a debit card at the gas pump. Since I no longer have to traipse to a job in Tempe — and because prices are so low now — gas bills have dropped to around $45 a month. That will increase, of course, as oil prices rise, but for the nonce, fuel for the car is within reason.

I could cancel Amazon Prime. But…it’s not very much, prorated monthly. And as I scribble, I’m sitting in front of an episode of Downton Abbey, which of course I’ve missed, in the absence of a television. Amazon’s offerings are better than Netflix, and it doesn’t seem to require software that won’t run on my computer or (so far) any other techno-weirdnesses. Since I have no other source of entertainment, it seems to0 bad to get rid of it.

But if it has to go…well, it just has to go.

Laundry can be soaked and washed by hand, and then run through the short, cold-water rinse & spin cycle. That will save a few pennies on electric and gas. I already hang most of the clothes to dry, so there’s not much to be saved there.

The dogs can do without their vaccinations. The vet’s office says they’re not due this year. And in fact, after they’ve had a number of shots, there’s really no need to keep getting more. Most of them confer lifelong immunity, or nearly so. At any rate, the problem is moot until this time next year. Thank heaven for small mercies.

Clothing is easy enough to cut — I surely don’t need any more right now. Future purchases can happen at My Sister’s Closet, a second-hand store fed by Scottsdale socialites. It carries some very nice examples of last year’s latest styles.

Eating out will have to go. There’s not much of that, but it has been sneaking in now and again. No more of it!

Groceries: No more frolics at Whole Foods. Food will have to come from Fry’s, Target, Walmart, and Safeway. There are a few things I’ll still need to get at Costco — chicken, for example, is usually cheaper there than anywhere else, and the pork, which is quite good, is rock bottom.

That’s about it. My lifestyle is already pretty frugal. It’s hard to see what more to cut without selling the house and moving somewhere cheaper to maintain.

And that, I hope to avoid…

Next step: to put this scheme into action.

Good Luck in this adventure. MAN….I thought it was just me BUT it is expensive to even live a fairly simple life now a days. I think the “bogey-man” in all this is Costco. I used to go to a full service grocery store and even when I used coupons, the costs just kept rising. I discovered Aldi and there “no non-sense” set up is great for us. I shop at Aldi once a week and shop at the full service place every 4-5 weeks. AND Aldi started accepting CC’s which is excellent for my rewards card (6%). Like you, our water bill rates continue to climb 7 to 10% a year with no apologies. But $45 for gas a month is excellent and $30 a month for your accountant…..A DEAL… Our biggest challenge continues to be keeping food from going bad…. Boy electric seems a bit expensive out your way…..

Yeah, Costco is the easiest target — none of those happy impulse buys are necessary for one’s survival. However, I think a bigger and hairier bogeyman is the cost of maintaining the house.

One could say I’m seriously house-poor here, between the maintenance & taxes on the paid-off house and, much worse, the $600/month I saddled myself with to buy the downtown house, back when I had a job and we thought my son would live there for five years, at the outside. He’s now been there for some 12 years and shows no sign of moving on. Nor, being a resident of a right-to-work state, is there any hope that he will ever earn enough to pay a $1200/month mortgage on one salary. The roommate thing was a horrible fiasco, and he shows no interest in marrying. So…. That looks like a forever thing.

We don’t have an Aldi here. There’s some other discount grocery store — it’s way up on the northwest side, a lengthy drive away. Now that you remind me, I’ll track that down and see if it’s worth schlepping up there.

My electric bill can drop to $80 in the winter. In the summer it’s high because keeping a house at 80 degrees on a 115-degree day puts quite a strain on any electric grid. My son, who lives in a different and far more rapacious company’s district, pays much, much more than I for electric.

Water is high in the summer because the damn city raises the rates over the summer. So even if you don’t consume any more water than you did in the winter, your water bill goes through the roof. And in 115 degrees, if you want to keep your shade trees alive, you DO consume more water.

Bear in mind that the S-corp also pays about $30/month for bookkeeping & tax accounting — so the total freight is about $60/month.

$60 a month ….. a bargain….I pay about that for a firm to do my taxes alone. To be clear I provide P & L print-outs as well as a breakdown of all income. My appointment takes about an hour….You are getting a bargain….IMHO. Both electric and water here is getting more expensive. The funny thing is the electric company claimed because people were using less electricity and buying efficient appliances ….they needed an increase…PAY MORE FOR LESS – makes perfect sense. The water bill increases are blamed on “new” government regs and compliance demands. Increases of 10% are routine. I am somewhat handy and therefore there is some savings BUT I have noticed the costs of everything has increased. This is magnified by repairs and maintenance on the rentals. I guess you should be grateful “the homestead” is paid off….Can you imagine your plight with a mortgage and a car payment? YIKES!!!

Your taxes are no doubt a lot more complicated than mine. WonderAccountant has access to my Quickbooks, and she does my bookkeeping in them now that QB has complicated its software so much I can’t use it anymore. I record checks & the like in Excel (since she doesn’t have access to my credit union’s online account, of course), so that she can identify what any given check or mystery transaction is about. QB automates about 80% of all that now, by sucking up data from the CU.

LOL! We’ve had power companies use the same ploy here to raise rates. Right now they’re preoccupied with trying to run rooftop solar leasing companies out of business. They succeeded in Nevada and now are trying to get rid of them here.

If I could afford 40 grand to install my own solar system on this house, I’d do it in a heartbeat….just to shove it to the power companies. And SRP is a great deal more benign than APS.

When I say I could’ve been living under the 7th Avenue Underpass during the Bush Recession, I’m not kidding. If the house hadn’t been paid off, I would have lost it — or else lost all my retirement savings, which would’ve had to go to keeping the roof over my head. And when I had a mortgage, payments weren’t that high — only about $800 a month. That was exactly half my net take-home pay at the time, and the only reason I was making ends meet was that SDXB was paying me rent and I was still getting alimony checks. Paying off the house was the smartest thing I did in the years immediately post-divorce.

The crazy thing is, $800 was about what it cost to rent an apartment back then. It’s twice that much here now. If I hadn’t had the paid-off roof, I can’t even imagine where I would have gone or what I would have done.

The sad thing is I see no glaring evidence of living beyond ones means in your or my lifestyle for that matter. But yet, like me, I seem to get the feeling you feel like you are “living on the edge” despite a pretty nice “safety net” to fall back on. I share your concerns on many levels. With poor returns on savings it seems the Fed in their efforts to prop up the economy are doing so at the expense of “savers” …ie…..seniors. As you aptly point out, there is no substitute for “a paid for home”….that peace of mind is priceless. BUT today’s environment is very tempting. I can borrow money in the form of a mortgage for 10 years at 2.25% with no points and may even get some help with closing for the effort. I just wonder sometimes how folks WITH … rent, a car payment, cell phone bills, student loans, utilities and child care make it….