Yesterday at the weekly Scottsdale Business Association meeting, the assertion was again made that you should never pay off a mortgage in advance. If you have the money to do so, we’re told, you’ll come out ahead if you invest the money in securities and keep making those mortgage payments.

I wonder about that.

Years ago, I paid off my $100,000 mortgage. (Can you believe I managed to wiggle into a North Central house for a hundred grand? Another recession was on: it was during the savings and loan fiasco.) The university had hired me into a full-time position, which though nontenurable, paid as much as an assistant professor in my department earned. SDXB was paying half the mortgage, which I carried on my books as rent, turning the many upgrades the house needed into tax deductions.

Years ago, I paid off my $100,000 mortgage. (Can you believe I managed to wiggle into a North Central house for a hundred grand? Another recession was on: it was during the savings and loan fiasco.) The university had hired me into a full-time position, which though nontenurable, paid as much as an assistant professor in my department earned. SDXB was paying half the mortgage, which I carried on my books as rent, turning the many upgrades the house needed into tax deductions.

With a year or two of alimony to go, it occurred to me that a) I would like SDXB to move out of my house and b) if I were covering the monthly mortgage payment myself, it would consume exactly half my net pay. Even with SDXB’s help, I was spending a little more than my entire net pay each month; if he left, I wouldn’t be able to stay in the house.

However, I had an inheritance from a distant relative, and I also had earned a chunk of dough by writing Math Magic for Scott Flansburg. With those amounts in hand, I could scrounge up the rest to pay off the mortgage from a couple of small investment accounts.

Over my investment adviser’s strenuous protests, I did it: Paid off the mortgage!

On several occasions, I’ve been glad I did it:

• It allowed me to show SDXB the door.

• After I was promoted to head up the university’s scholarly editing project, the increase in salary allowed me to stash a lot of money back into savings, thanks to the absence of an onerous mortgage payment.

• When I was laid off the job, I was able to hang onto the house, which would not have happened if I’d had to make mortgage payments.

Because the value of the house was pretty small, in the larger scheme of things, the tax effects of getting quit of the mortgage were nil. Maybe if the house had been worth half a million bucks or so, or maybe if I were earning a living wage, it would have made a difference. But in my circumstances, it did not.

But the question keeps coming back to haunt: was it a mistake to pay off that mortgage?

So I applied a little English-Major Math to the issue. Here’s what I came up with:

Let us imagine you can buy a house for $100,000. You can finance it at 3.5% with no down payment (it’s before the Bubble, OK?). Incidentally, you happen to have $300,000 laying around in investments; of that, about $150,000 is not in tax-deferred instruments.

What would happen if you…

a) paid the $100,000 to a lender over 30 years; or

b) paid off the $100,000 in one swell foop?

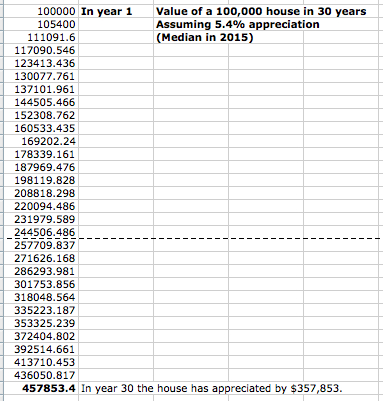

In 30 years at a 5.4% appreciation rate, your $100,000 shack will be worth $436,050. Subtract the Year 1 value of $100,000, which you paid in cash, and your net value for your house will be $336,050.

If you took that $100,000 and instead invested it in an index fund returning about 5% p.a., on average, after 30 years that fund would be worth $411,613.

At a glance, it looks like you’d do better to put the 100 grand in savings than into the house.

However…that doesn’t take into consideration the real cost of a $100,000 mortgage over 30 years.

According to Bankrate, the total interest and principal you’ll pay on that 30-year mortgage at 3.5% comes to $161,657 — not including tax and insurance. Again, it looks like we’ll do better to put the cash in a nice, calm index fund.

So, let’s think about that:

At the end of 30 years, you’ve paid $161,657 to buy a house that is now worth $457,853. The net value of the house ($437,853 valuation minus $161,657 total interest and principal payments) is $296,196.

If you had not financed the house but paid for it with $100,000 out of pocket, your net value for the house after 30 years is 357,853 (i.e., $457,853 – $100,000).

Okay, keep these figures in mind:

Finance the house: net $296,196 on sale of house 30 years later

Pay off the house: net $357,853 on sale of house 30 years later

Even though paying off the house looks better, these figures still make the $411,613 that could now be sitting in your index fund look very good. Sell the house for $296,196, and you end up with an admirable enough $707,809.

HoweEVER: what if you figured that if you could afford to fork over a monthly PITI payment to a mortgage company in the amount of about $625, you could afford to stash that amount in savings — after you’ve paid off the house?

If you invested $625 a month in a low-load index fund (Vanguard has two of them), in 30 years you would have $357,853. Let’s suppose you have the foresight to do exactly that: you pay your $100,000 in cash, and you invest the equivalent of the house payments over the course of 30 years.

Now you have a total of $769,466 ($357,853 + 411,613). That is $60,000 more than you would have had if you’d paid that $625 a month to a lender.

These prognostications depend strongly on interest rates. Mortgage rates are still very low just now — at the present 3.4%, it makes sense to buy a house with as large a home loan as you can get. But once rates rise above about 5 percent, that changes.

Over the past 30 years, the average 30-year fixed mortgage rate has been 7.19%. At times, it’s risen over an eye-popping 16%. The present extended period of cheap money pushes that average to a deceptively low level.

At 7.19% interest, your principal and interest payments on $100,000 would add up to $244,122 over 30 years. Now the net value of the house to you is $193,731 (i.e., $437,853 – 244,122). That doesn’t compare well at all with the $357,853 you would net on the house had you paid out that $100,000 lo these many years ago.

So, here are four strategies, in the order of effectiveness — from most profitable to least profitable.

1. Pay off the $100,000, then invest the equivalent of principal & interest payments at 5% (your net after 30 years: $594,103: value of house + value of index fund)

2. Finance the $100,000 at 3.5%; invest the amount of the monthly mortgage payments in a low-cost index fund (you end up with $532,446)

3. Pay the $100,000; spend the payment amounts to support a better lifestyle ($336,050)

4. Finance the $100,000 with a conventional 30-year fixed-rate mortgage at 3.5% and pay principal and interest until you’re ready to fall into the grave ($296,196)

Disclaimer: Don’t believe things you read on random websites! I am not a financial advisor. I am an aging English major who prefers playing with Excel to solving crossword puzzles. None of the above constitutes or is intended to constitute financial advice.