All right. It’s true: I’ve neglected the budgeting over the past some months. Years. WhatEVER. More interesting obsessions came along, and I got bored with entering every little purchase in a spreadsheet by way of keeping the spending within bounds.

The thing is, when you do that, it does help to keep your spending under control. When you realize you have enough money to get by in the manner to which you have frugally accustomed yourself and so you decide to quit with the minutiae, that’s when your spending gets out of control.

The whole stupid Costco credit card thing and the adjunct concern about having to use my debit card or checkbook to shop there led me to think about how much money I actually spend at Costco.

How much DO I spend there, anyway? And what if I stopped buying things at Costco altogether, it being the Mother of All Impulse Buy Vendors: would monthly expenditures drop?

Conveniently, the last time Intuit “updated” its online Quickbooks, they put it way beyond my meager techno-skills. I can’t use it at all, and only keep my accounts there for WonderAccountant’s convenience. So — here’s the convenient part — I happen to have an Excel workbook in which I’ve been keeping a shadow account of debits and credits, so that W.A. can tell who checks have been written to and what for. And come the end of May, six months of said debits and credits were neatly recorded.

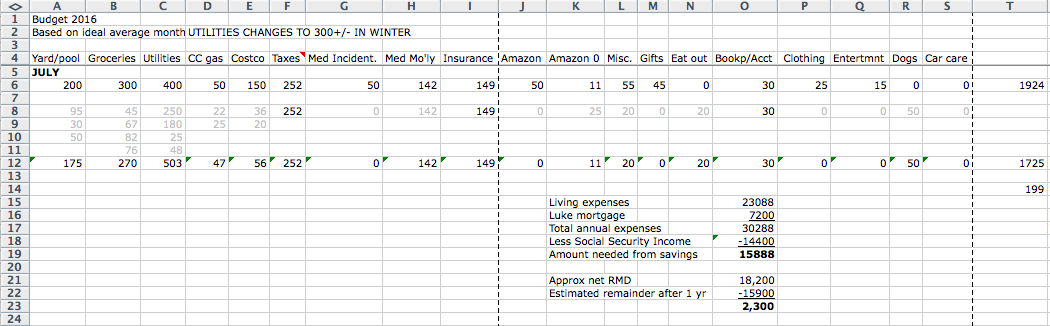

Ergo…it was very easy to create a spreadsheet showing all expenditures of every variety and then sort them by vendor and by category. Then I averaged expenditures for each category over six months. What I discovered was pretty amazing.

The largest monthly expense, not surprisingly, is my share of the mortgage on the house my son and I co-own in lovely central Phoenix. That’s not something I can do much about, although it is a bone of contention with the financial advisor, who hates it.

Over the past six months, maintenance of the house and pool have racked up the highest average monthly expenditure (i.e., total up all the costs and divide by 6). Four reasons for that:

• The $758 bill for the pool pump repair

• A couple hundred bucks on new shelving for the work shed, much needed

• And, after two years of neglect, I decided to buy plants and several beautiful (expensive!) Talevera pots to revive the outdoor sitting areas and gardens where I like to hang out.

• There was a plumber’s bill in there, too…

Groceries, at an exorbitant $396, run a distant second to the house & pool. That’s even more astonishing than it seems, because in fact I buy most of my food, household products, and personal products at Costco.

There are two categories for tax-deductible medical bills: Med 1 (a) comprises one-time purchases — a prescription, for example, or a dentist’s visit. Med 1 Annual covers Medigap (Medicare supplemental insurance), Medicare Part D (prescription drugs), and long-term care insurance. If you combined those two categories into one, medical costs would come in third, after groceries, at a breathtaking $335 a month.

Costco, then, at “only” $283 a month, is actually fourth in average monthly expenditures. Without the pool pump repair, it probably would move up a notch, to third — any way you look at it, homeownership ain’t cheap.

Total expenditures for the house insurance, the car insurance, and an umbrella policy average $149 a month, probably not too exorbitant in context with the other spending categories. Once you get past those top eight expenses (mortgage through insurance), other spending is fairly modest.

Can you believe that $3 average over six months of car maintenance? 😀 I forgot to take the Dog Chariot in for its oil change between December and May! It’s still running. There is no freaking way I’m buying a new car!!!!! When it falls apart, I’m trading the pile of metal in on a mule.

So…when you add it all up, if you include the mortgage on the communal house, I’m spending $3140 a month, significantly more than I can afford. Without the mortgage (which is paid from funds I don’t use to live on), my actual living expenses come to $2540 a month.

Since my net Social Security income is $1200 a month, that would seem to pose something of a problem…

In fact, in the absence of the adjunct teaching income, I use a portion of the annual RMD (required minimum withdrawal) from a large IRA to live on, but when you include the $600 for the downtown house, you come up with a total spending figure just about equivalent to the entire RMD.

Since I would like to be able to reinvest as much as I can of that RMD, pretty clearly I’m going to have to cut expenses.

⇒ The $396 on groceries is the first candidate in that department. It’s pretty inexplicable. Presumably it’s happening because I shop a lot at Whole Foods and at AJ’s, a local fancy grocery store. I’m not buying much of the dog food in grocery stores — Costco has good prices on chicken and especially on pork. I did start buying a fair amount of my meat at WF and AJ’s, because their offerings are far superior to anyone else’s, at least most of the time.

As a matter of fact, though, yesterday I picked up a spectacular grass-fed Black Angus steak from the quick-sale shelf at the Safeway: 30% off an already discounted price. If I would bestir myself to stumble into Safeway at the right time of day on the right day of the week, I could stock the freezer a lot more cheaply than I do.

⇒ I can’t do a lot about the utilities. Even though that entry ranks among the highest, the figure you see there is pretty modest — it reflects the winter months, when I don’t run either AC or heat and when not much water is needed to keep the xeric landscaping alive. Over the summer, it’ll be almost twice that much.

⇒ Gasoline is pretty cheap, between the low prices and the fact that I don’t have to drive across the city to go to work anymore. I hardly drive at all, really. As long as prices stay down, a $50 cash card from Costco will cover that monthly budget item. That obviates the problem of how I’m going to buy cheap Costco gas without their hateworthy new CitiGroup Visa card.

⇒ Then we have the issue of the medical costs. For older Americans, this is often — maybe we should say “typically” — one of the largest expenses. The older you get, the more things go wrong with you. And Medicare, though it’s a big improvement over Obamacare, isn’t cheap. Especially when you’re permanently unemployed.

⇒ A big bugaboo for all of us old folks is long-term care. A nursing home can pauperize you in a matter of months — one hopes to die before one gets sucked into one of those places. While I was working at ASU, I bought long-term care insurance, but after I was laid off the job I lost the right (heh!) to increase the monthly payments so as to have the insurance payout keep up with inflation. That hasn’t discouraged the company from raising its premiums by bracing amounts each year, so that now I’m paying $132 a month for insurance that will not cover me if I’m unfortunate enough to get locked up in one of those places.

That’s $1582 a year. Supposing that I manage to stay out of nursing care until I’m 80 — another 10 years — if I were to put that much into a savings account, I’d have $15,820 to fork over to custodians.

Right now, today, the typical cost of a nursing home in this area ranges from $2232 to $6572 a month. God only knows what it’ll be in 10 years. Lower-end homes are real holes, so figure that if you’re lucky, you’ll spend maybe $4000 to $5000 a month — today. That’s $48,000 to $60,000 a year!

Obviously, 10 years of savings accrued by canceling the long-term care policy and banking the premiums wouldn’t cut it.

Most people don’t spend years in nursing homes. They either recover and go home after a few months or, with any luck, die within a few months.

But… Oh, yes.

But: some people end up in those places for month after month and year after year. The proprietors clean their pockets of every single asset they have, forcing them to sell their homes, cars, stocks, artwork — everything — to keep themselves in an institution. Then, once the person is utterly destitute, the state takes over…but that means moving you into one of the low-end holes the inside of which we would all hope never to see.

If you’re one of the “most people,” then obviously long-term care insurance is not the best of all possible bets. But if you’re among the unlucky — and the woods are full of them — then LTC coverage will stave off the evil day that you’re completely broke, keeping you in a halfway decent place until you die. Unless, of course, you’re very unlucky, indeed.

It’s a gamble: one in which you bet against an insurance company that you’re going to lose in the game of life.

So, reflecting on this state of affairs, I gazed upon the spreadsheet and wondered where I can cut costs.

Number 1: I’d like to try staying out of Costco for the next six months, just to see what happens. I might go in there to pick up the lifetime supplies of toilet paper and paper towels — it’s such a luxury not to have to buy those things every time you turn around.

It’s a little hard for me to believe the grocery bills would go up if I quit buying things in Costco, especially if I would stick to Fry’s and Safeway for food and household items.

Amazon seems to be soaking up rather more money than one would desire. I could cancel the Amazon Prime — and why are they gouging me for something called “digital services” when I’ve never even been able to figure out how to download a movie from their cloud??? It would take a lot more Amazon orders than I make to save the equivalent of the monthly cost for Amazon Prime.

Shopping a little more consciously would cut the grocery bills. In the past I’ve cut routine bills simply by being aware that I need to be careful and by keeping close track of how much I’m spending, and where. I should be able to cut at least $100 from the cost of grocery-store junkets.

I could go back to the habit of never eating in restaurants. Period. Doesn’t seem like a $35 saving really justifies never, ever eating out. But…maybe. Every little bit helps.

If I drop the long-term care insurance, that will save $132 a month. But I think the commensurate risk would be unacceptable.

The only way to cut the really big expenses — house and pool, taxes, insurance — would be to move out of this house. A place without a pool would still require maintenance, but not as much. If I moved to Sun City, property taxes would drop by two-thirds and insurance would drop by half. However, utilities would rise, probably by 50% to 100%: Sun City is served by the rapacious Arizona Public Service, whose power bills are extortionate. Those houses out there were built before power cost much, and so they’re poorly insulated and expensive to air-condition.

And of course, we do have to deal with the fact that I don’t WANT to live in Sun City.

So WTF? Do I have a plan?

Yeah.

- Avoid Costco. Buy a cash card once a month for gasoline, and while there pick up a month’s worth of dog meat and restock paper goods as needed.

- Also stay out of Whole Foods. Purchase “organic” frou-frou at Trader Joe’s and Sprouts. Buy more food and household items at Fry’s, Target, and the new neighborhood Walmart down the street.

- Don’t buy any more clothes of any description.

- Next time an expensive repair happens to that pool pump, replace the thing.

- Quit eating in restaurants.

- Keep track of expenditures on a weekly basis. Budget specific amounts for categories and try to stay on budget.

- Dump the Amazon Digital, whatever that is.

If I could spend $240 a month less, that would bring my living expenses down to $2300: equivalent of my net Social Security plus net former adjunct earnings ($1100, prorated over 12 months). If The Copyeditor’s Desk keeps chugging along the way it has of late, it can disburse $1100 a month, allowing me to live on SS plus earned income.

Then the only part of the RMD that would be consumed would be the $600 a month for the downtown house, and that would leave a substantial amount of the RMD, after taxes, to reinvest in savings instruments.